In 2022, the conforming loan limit for a single-family home is $647,200 in most of the U.S. But that number is expected to change on November 30 when the FHFA announces new conforming loan limits for 2023. The new “baseline” limit is likely to be over $700,000 across most of the U.S. And in high-cost markets, loan limits should be over $1 million.

Increasing loan limits will help buyers get better mortgage rates and make smaller down payments on loan amounts over $647,200. And some buyers won’t have to wait until 2023 for those benefits. Select mortgage lenders are already offering higher loan limits in anticipation of the FHFA’s official change.

Expected conforming loan limits for 2023

Each year, the FHFA adjusts conforming loan limits for mortgages backed by Fannie Mae and Freddie Mac. Loan limits for the next year reflect average U.S. home prices for the third quarter of the current year. So if home prices have risen, loan limits will be increased by a similar margin.

Although the third quarter of 2022 has yet to end, the national median sales price for the second quarter increased nearly 18% from the previous year. That means 2023 loan limits should see a sizeable increase, too. And some mortgage lenders are getting a head start by increasing their loan limits before the end of the year.

If you’re buying a home with a mortgage above the current loan limit, you don’t need to wait until next year. Start shopping around for lenders today that have already increased their loan limits.

Last week, Rocket Mortgage and United Wholesale Mortgage (UWM) both announced they were increasing their loan limits to $715,000. They were quickly followed by PennyMac and Finance of America.

While some experts predict new conforming limits could be higher — near the mid-$700,000s — other lenders are likely to follow suit by increasing their limits to $715,000 before the end of the year.

By raising their conforming loan limits early, these lenders are essentially offering a discount for purchase, refinance, or cash-out refinance loans between $647,201 and $715,000. Doing so gives them an edge over their competition ahead of the FHFA announcement for all lenders in November.

How conforming loan limits are set

The calculation for conforming loan limits is based on average U.S. home price increases for the previous year in the FHFA House Price Index.

Looking at the latest figures from FHFA, another double-digit jump in the loan limit appears to be coming. If we use second-quarter numbers as an estimate, the conforming loan limit ceiling would rise 12%, to nearly $725,000. In high-cost areas, that ceiling would pass the million-dollar benchmark.

The Housing and Economic Recovery Act of 2008 established a formula that required any increase to conforming loan limits could only happen after home prices returned to pre-recession levels. That condition was met eight years later in 2016 when the FHFA increased the conforming limits for the first time in 10 years.

What about FHA and VA loan limits for 2023?

Technically, there are no loan limits for VA loans, meaning lenders can lend any amount for which the borrower qualifies. There are only limits to how much the VA will guarantee. VA loan limits are typically defined as the amount you can borrow without having to make a down payment.

Where loan limits apply, VA loans often utilize conforming loan limits. That means, if conforming loans are increased to $715,000, eligible VA mortgage borrowers will likely be able to borrow up to $715,000 without having to make a down payment.

FHA loans do enforce specific loan limits, which are lower than conforming loan limits. But they are calculated based on FHFA’s guidelines and should increase next year in tandem with conforming loans. As such, there’s a good chance the standard FHA loan limit will be over $520,000 in 2023.

What do higher mortgage loan limits mean for you

The loan limit is a key benchmark for mortgage borrowers as well as lenders. It is the maximum dollar amount on mortgages that can be acquired by government-sponsored enterprises Fannie Mae and Freddie Mac.

Anything over the conforming loan limit is considered a jumbo loan, which typically means higher interest rates and bigger down payment requirements. Loans within the conforming mortgage limit get to enjoy low down payments and competitive interest rates thanks to their backing from Fannie and Freddie.

According to Brett DePriest, Sr. Vice President of Acopia Home Loans, “Home buyers won’t need 10-20% down, or have to take out equity lines for higher priced homes. The ability to purchase a $759,000 home with just 5% down should make buying a home in this price point more affordable, opening the market to more buyers.”

More lenders are expected to follow suit by increasing their conforming limits ahead of the FHFA announcement on Nov. 30. If you’re buying a home and your loan amount falls in this range, you don’t need to wait until next year. Start shopping around for lenders today that have already increased their loan limits.

The best loan for home renovations depends on your situation. If you want to buy and renovate a fixer-upper, options like the HomeStyle loan, CHOICERenovation loan, or FHA 203k rehab loan could be ideal. If you already own your home and want to make improvements, tapping your equity with a cash-out refinance, home equity loan, or HELOC could be better.

It’s important to choose the right renovation loan based on your project and your finances. Here’s what you should know about your options.

What is a renovation loan?

Typically, a home renovation loan is a single mortgage that lets you both finance a home and renovate it. Renovation loans can be used either when buying a home or refinancing one you already own. By financing the home and the renovations together, you can consolidate your renovation costs into one low-rate mortgage rather than taking out separate loans to buy the property and pay for repairs.

How does a renovation loan work?

Renovation loans are unique because they let you borrow more than the home’s current value. Typically, the maximum loan amount is your home’s estimated future value after renovations are complete.

You’ll need detailed construction plans and cost estimates to qualify for a renovation loan. Having inspected the property and reviewed your plans and contractor quotes, the home appraiser will give an “as improved” valuation. Assuming the project is viable, you get the mortgage portion of your loan right away so you can complete the purchase or refinance.

Renovation funds are then released in stages (“draws”) as your project reaches pre-agreed milestones. You’ll need a contractor that’s happy working on that basis. It typically helps to find a contractor who has worked with renovation loan programs in the past and understands how the process should go.

Renovation loans to buy and fix up a home

Most mainstream mortgage programs have a renovation loan option. Conforming loan programs including Fannie Mae’s HomeStyle Renovation and Freddie Mac’s CHOICERenovation. Government-backed renovation loans include the FHA 203k mortgage, the VA renovation loan, and the USDA renovation loan. Note that the VA and USDA renovation options are less common and it may be hard to find a participating lender.

Let’s dig into each renovation loan in a little more detail.

Fannie Mae HomeStyle renovation loan

Fannie Mae’s HomeStyle renovation loan is fairly easy to qualify for. You need at least a 3% down payment, a reasonable debt-to-income ratio, and a minimum credit score of 620 (although this can vary by lender).

HomeStyle can be used to buy and renovate a new home or refinance and upgrade a home you currently own. There are few restrictions on how the funds can be used, although you are not allowed to knock down the existing property and build a new one (for that, you’d need a new construction loan).

Freddie Mac CHOICERenovation loan

Like Fannie Mae’s HomeStyle loan, Freddie Mac’s ChoiceRENOVATION loan is a conforming mortgage. And the two loan programs are almost identical. To qualify, you need a 3-5% down payment and a credit score of 620-660 or higher, depending on your mortgage lender. Like the HomeStyle program, CHOICERenovation allows you to either buy a home or refinance one you already own.

However, there is one important difference. The CHOICERenovation mortgage lets you finance improvements to your home’s resilience (think disaster proofing) while HomeStyle does not.

The big advantage of a HomeStyle or CHOICERenovation loan over an FHA 203k loan concerns mortgage insurance. FHA loans typically have permanent mortgage insurance that you can only get out of by paying off your mortgage, refinancing, or selling. But, with Fannie and Freddie loans, you can remove PMI payments when your equity reaches 20% of the home’s value. That can lead to big savings over the long term.

FHA 203k loan

The FHA 203k rehabilitation loan is a government-backed renovation mortgage. It can be great for those with slightly lower credit because most lenders require only a 580 FICO score to qualify for an FHA loan. The “Limited” FHA 203k loan allows up to $35,000 in renovation costs while the “Standard” FHA 203k allows you to borrow up to local FHA loan limits. Keep in mind that these loans cannot be used for luxury amenities like swimming pools.

The FHA 203k rehab loan comes with two main disadvantages compared to conforming loans:

Its minimum down payment is 3.5%, versus 3% for a HomeStyle or CHOICERenovation loan

FHA mortgage insurance typically lasts the life of the loan, while conventional private mortgage insurance (PMI) can be removed later on

If your credit score is high enough for a Fannie Mae or Freddie Mac renovation loan, it’s worth looking into these options first as you could save money on interest rates and mortgage insurance.

VA renovation loan

The VA renovation loan is only available to qualified service members, veterans, and select military-related groups. But it can offer real benefits to those who are eligible, including:

No down payment required

No ongoing mortgage insurance payments (just a one-time VA funding fee)

VA mortgage rates are usually lower than conforming and FHA loan rates

If you’re eligible for a VA loan, these are typically the best mortgages. However, not all lenders offer VA renovation loans, so be prepared to put in some effort to track one down.

USDA renovation loan

The USDA renovation loan is available only to those purchasing a home in an area designated as “rural” by the U.S. Department of Agriculture. However, that definition is broader than many expect. You don’t need to work in agriculture or use the land for farming purposes and roughly 97% of America’s land mass is eligible.

The big advantage of USDA loans is that you don’t need a down payment. But you will need a low-to-average income to qualify. Other benefits include below-market mortgage rates and reduced mortgage insurance rates.

Like the VA renovation loan, however, USDA renovation loans are hard to come by. So you should expect to do some research if you want to find a lender offering this program.

Renovation loans for a home you already own

If you already own your home, a “true” renovation loan is not your only option. In fact, it may be easier and cheaper to borrow from your equity using a cash-out refinance, home equity loan, or home equity line of credit (HELOC).

These loans provide cash that you can use for any purpose, meaning you don’t need to have detailed construction plans and contractor quotes in order to qualify. You only need to qualify for the loan based on your credit, income, and available equity; then you can use the money for any type of renovation you want.

Also, the interest you pay on a cash-out refinance or home equity loan may be tax-deductible if you spend the money on home improvements. But you should check with a tax professional to see whether that applies to you and how much interest would be deductible.

Cash-out refinance

With a cash-out refinance, you get a whole new mortgage that replaces your existing home loan. Your new loan balance will be higher than your old balance, and you’ll receive the difference (minus closing costs) as your cash-back. Conforming and FHA loans typically let you borrow up to 80% of your home’s value using a cash-out refinance, while VA loans allow you to borrow 100% of your equity. USDA loans don’t allow cash-out refinancing.

When mortgage rates are low, a cash-out refinance is the go-to solution for many homeowners. It can allow you to cash out equity and secure a better interest rate on your home loan at the same time. But mortgage rates are now higher than they were a couple of years ago, and you should always think twice before refinancing to a higher rate. Run the figures carefully before you decide.

In addition, a cash-out refinance can come with high closing costs. Your lender may offer to cover some or all those costs, but you’ll almost invariably pay a higher mortgage rate if it does.

Home equity loan or HELOC

With a home equity loan, you get a second mortgage and leave your existing one in place. You’ll receive a lump sum at closing, which you repay in equal installments over the “term” (duration) of the loan. Usually, these loans come with fixed interest rates. Home equity loan rates are typically higher compared to a cash-out refinance, but your closing costs should be way lower.

A home equity line of credit (HELOC) is another form of a second mortgage. But it acts more like a credit card: You can borrow from the line, repay it, and reborrow as often as you want up to your credit limit. And you pay interest only on your balance. After a draw period during which you can borrow from the HELOC, you’ll enter a repayment period when you can no longer borrow and must repay your outstanding loan balance in full.

That could make a HELOC ideal if you have a drawn-out renovation project (or multiple projects) that will happen over an extended period of time. You can borrow funds as needed and you won’t pay interest on the money you’re not actively using. But HELOCs can be complicated. To learn more about HELOC’s pros and cons and explore all your options before applying.

How do I finance home renovations without equity?

All the loan options above — including renovation loans, cash-out refinancing, and home equity loans — allow you to finance home improvements using your home’s value (your equity) as security. This is often a good option because financing secured by your home is cheaper than other forms of borrowing. But there are risks, too. You’re putting your home on the line if things go badly wrong. Ultimately, if you default on a loan secured on your home, you could face foreclosure.

Depending on your circumstances, you might prefer to avoid that risk. And you may be willing to pay a higher interest rate to do so, especially if your renovations have a relatively modest budget.

Your main choices then are getting a personal loan or using your credit cards.

You may see personal loans advertised at rates that rival or even undercut those for home equity loans and HELOCs. But be aware that few applicants are approved at those rates. You’d need an exceptional credit score and very sound finances to qualify. If that’s not you, expect to pay an appreciably higher rate than on secured loans.

Credit cards usually have much higher interest rates than secured loans. So you wouldn’t want to finance extensive home renovations using plastic. One possibility is using a card with a 0% rate for an introductory period that often lasts 18 or 21 months. Then you could pay off the card or transfer its balance before you begin to pay interest. But, if you’re buying a home, don’t apply before you close or you could risk hurting your credit score and your chances of mortgage approval. And never apply for more than one card within a short period of time.

Renovation loan FAQ

Can you renovate a house with a loan?

Yes! There are a variety of loan options that can be used for home renovations. Those buying a fixer-upper home might consider the Fannie Mae HomeStyle loan, Freddie Mac CHOICERenovation loan, or FHA 203k rehabilitation loan. Current homeowners often finance renovations using a cash-out refinance, home equity loan, or HELOC. And if you don’t want to touch your home’s equity (or don’t qualify for the mortgage), a personal loan could be an option.

Do renovation loans have higher interest rates?

Yes, most renovation loans have slightly higher rates. From a lender’s point of view, these loans carry a little more risk. However, rates for these tend to be only slightly higher than those for purchase-only mortgages. You’ll see the difference when you start to compare shop for your loan.

What is an FHA 203k loan?

The FHA 203k rehab loan is a government-backed renovation loan. It allows you to buy or refinance a property and includes the cost of renovations in your loan amount. The FHA 203k program can be a great choice for those with credit scores of 580-620. But you may find other alternatives more attractive if you have a strong credit score.

What documents are required for a renovation loan?

Renovation loans involve more documentation than purchase-only mortgages In addition to the standard application paperwork (like bank statements and income documentation), expect to provide construction plans, contractor quotes and specifications, work schedules, local authority permits, and anything else the appraiser needs to ensure your project is viable.

What is the maximum renovation loan amount?

That varies between programs, lenders, and projects. If you’re using a renovation loan to buy and fix up a property, you can often borrow up to the home’s future value — its estimated cost after renovations are completed. But your loan amount will have to fall with local conforming or FHA loan limits. Those using a cash-out refinance, home equity loan or HELOC can often borrow up to 80 or 85 percent of their property value, minus their current mortgage amount.

How do I get a renovation loan?

Most renovation loans are offered through mortgage lenders, just like standard home buying and refinance loans. But the process is different. To apply, you’ll need detailed renovation plans and cost estimates in addition to the usual financial documentation. Once you decide on a loan program, reach out to a mortgage lender to find out exactly how the process works and what documentation you should prepare.

Which renovation loan is best for you?

As you can see, there’s a wide variety of renovation loans available. The best program for you depends on a number of factors, like whether you’re buying a fixer-upper or renovating a home you currently own, and what kind of shape your finances are in. Your best bet is to connect with a lender and discuss options. Your mortgage loan officer can help evaluate your plans and financial situation to determine which renovation loan is best.

A home appraisal determines the fair market value of a property and helps ensure you don’t overpay for it. Appraisals protect both the buyer and the mortgage lender, and most loan programs require one when you purchase a new home.

Most borrowers pay between $300 and $425 for a home appraisal, which is included in their closing costs. But, if you meet certain guidelines, you may not need one when refinancing a home you already own.

Keep reading to learn more about appraisal costs, what to expect from the process, and why it’s important for your home-buying journey.

What is a home appraisal?

A home appraisal is used to determine a property’s “true” value. Professional real estate appraisers inspect a home’s condition and features, then compare it to recently sold homes in the nearby housing market. The appraiser will judge how different factors — like plot, location, upgrades, amenities, and square footage — impact your home’s value when compared to other similar properties (called “comps”). Ultimately, appraisers come up with a fair market value for the home.

Why are home appraisals required?

Lenders usually require an appraisal because they want to be certain the home is worth its purchase price and could be sold to cover losses if you default on your mortgage. Mortgage lenders will not give you a mortgage loan above the appraised home value because that would put them at risk of financial loss in the event of a foreclosure.

Your lender will order the home appraisal during the mortgage approval process, but won’t ultimately pay for it. It’s typically the home buyer who pays the appraisal fee. However, in some areas, the seller traditionally picks up the tab.

Are a home appraisal and home inspection the same thing?

First-time home buyers may confuse a home appraisal with a home inspection. Both occur before a home purchase and give a buyer the opportunity to back out of the sale or renegotiate. However, the two are inherently different.

A home inspection is an in-depth examination of a property’s HVAC, plumbing, foundation, and other systems, rather than an estimation of a home’s value. Inspections are meant to turn up any structural or functional issues with a home prior to the sale, giving buyers a chance to renegotiate the purchase price or ask the seller to make repairs. In addition, a home appraisal is almost always required by mortgage lenders whereas an inspection is optional (but highly recommended).

How much does a home appraisal cost?

A typical appraisal for a single-family home costs around $350, with average prices ranging between $313 and $421, according to research conducted by HomeAdvisor. But prices vary by location. For example, California home buyers can expect their home appraisals to cost anywhere from $600 to $800. In addition, variables such as the time of year and size of the property can affect home appraisal fees. Indeed, a multifamily home appraisal can cost upwards of $1,500.

Typically, you’ll be lucky to pay less than $300 for an appraisal and unlucky to pay more than $450. However, if you require a particularly detailed report on an exceptionally large home with complex valuation issues, you could easily end up paying four figures.

How appraisals help buyers

Many buyers see appraisals as undesirable. At best, they’re yet another charge on a long list that makes up closing costs. At worst, a low appraisal can torpedo a deal, snatching a dream home from a keen buyer.

However, there’s another way of looking at home appraisals. They stop you from paying too much for a property. And why would you want to pay over the fair market value for your next home?

As importantly, many home buyers use a low appraisal to renegotiate the purchase price. That can equal savings greater than the appraiser’s fee. On the other hand, a higher appraised value can give buyers more home equity and a good deal on the property.

What does an appraiser look for?

Many real estate appraisers use the Fannie Mae Uniform Residential Appraisal Report to assess the condition of a property. Here are some of the things appraisers consider when comparing a home’s asking price to its true value:

The living condition of the home: An appraiser will evaluate the general condition of the property. They’ll count the number of bedrooms and bathrooms, assess the floor plan’s functionality, look at home amenities, and confirm the square footage

Home improvements: The appraiser will consider any home renovations or other upgrades to the property that may improve the value of your home. They’ll also appraise any improvements made outside of the home, such as new landscaping, a pool, or a renovated garage

Nearby home values: A licensed appraiser will also evaluate comparable properties, or “comps,” in the nearby housing market. They’ll look at the sale price of other homes and their current property values to determine the appraised value of your new home

Once the appraiser completes their evaluation, they’ll issue a final valuation of the property in an appraisal report that is submitted to your mortgage lender.

What’s included in an appraisal report?

Typically, a home appraisal report includes:

Explanation of the valuation: Appraisers show their work so you know how they arrived at the home’s final value

A brief overview of local housing market trends: Are prices currently going up or down? If so, how quickly?

Summary of the home’s characteristics: Its condition, size, and any improvements that have been carried out

Other considerations: Has anything else about the home or its neighborhood affected the valuation?

Structural problems and defects: Any issues that the appraiser noticed that affected their valuation

It’s important to recognize that home appraisers are not home inspectors. Don’t rely on their expertise to uncover structural problems because they won’t always discover those. In any event, it’s not their job to look for these types of issues.

Appraisers typically value your property in several ways. The most common is the “comparables” valuation detailed above, which finds a value by comparing the subject property to other nearby sales. The “replacement cost” is what it would take to replace the home on the same lot. And the “rental schedule” arrives at the value by considering rental income.

What sellers provide during the home appraisal process

The National Association of Realtors recommends that real estate agents and sellers should prepare a package of documents and make it available to appraisers when they arrive for the inspection. The NAR suggests that the package should contain copies of as many as possible of the following:

Detailed maps of the near neighborhood plats

Surveys

Deeds

Covenants

HOA documents

Floor plans

Specifications

Inspection reports

Neighborhood Details

Recent comparable sales

Detailed list and dates of upgrades, home improvements, and costs, with invoices where possible

Energy-efficient green features

Purchase agreement

The more of those a seller and real estate agent provide, the more accurate the appraisal might be.

Cash buyers don’t need a home appraisal

Not all real estate transactions require a home appraisal. People buying a home with their own cash aren’t obliged to have one.

Also, professional developers rarely bother. They reckon they know as much as any appraiser. And, anyway, what’s the point of establishing the market value of a home if you’re going to tear it down and build a new one? You just need to know the going rate for development land.

Refinancing doesn’t always require an appraisal

Mainstream mortgage lenders typically require a property appraisal when you’re buying a home. But they sometimes won’t insist on one when you’re refinancing. “If you have 20% down, then you do not always need an appraisal — even for some home purchases,” says Jon Meyer, The Mortgage Reports loan expert and licensed MLO.

It’s up to your lender. However, the general rule is that appraisals aren’t always needed when the total amount of the loan being refinanced is $250,000 or less.

Homeowners with an FHA loan can refinance without a home appraisal using the FHA Streamline Refinance program. Similarly, borrowers with a VA loan can use the Interest Rate Reduction Refinance Loan (IRRRL) without an appraisal.

Lenders are least likely to require an appraisal for a conventional mortgage loan when you want a “rate-and-term” refinance. That means you pay your closing costs out of pocket and improve on your mortgage terms without increasing the balance. If you wrap the refinance costs into a new loan, it’s called a “limited cash-out” home loan.

Lenders are most likely to require an appraisal when your loan-to-value ratio (LTV) exceeds 80% or when you apply for a cash-out refinance.

Dos and don’ts on home appraisal day

Sellers and agents may attend the home appraisal. However, they should only answer questions and provide information. Trying to influence the appraisal outcome in any way is illegal.

The appraiser is not allowed to divulge anything confidential at this point. You may, however, ask to check the appraiser’s credentials and satisfy yourself that they have the requisite local knowledge to reach a fair valuation. That’s important, because some appraisers jump at any opportunity to grab a job, even if they do not know the area.

So it’s a good idea to check the office address and make sure it isn’t in the next county. If you have well-founded doubts about either the appraiser’s knowledge or credentials, you can ask the lender to send someone else.

Such situations are relatively rare. Most appraisers strive to deliver exactly what they’re paid for: a valuation that reflects the fair market value of the home.

Home appraisal FAQ

What’s the purpose of a home appraisal?

The purpose of a home appraisal is to establish the fair market value of a home. It confirms for both you and your mortgage lender that the agreed price of the property is reasonable. An appraisal also ensures that a borrower is within loan-to-value guidelines. When an appraisal comes in low, the buyer may need to increase their down payment to qualify for the home loan. Furthermore, in some states, home appraisals may be used to calculate property taxes.

What will fail a home appraisal?

A home appraisal fails when it issues an appraised value that is less than the home purchase price. Several factors can fail a home appraisal, including sluggish housing market conditions, bad comps, and inexperienced appraisers who don’t possess adequate local market knowledge. Messy and blighted homes can also fail an appraisal. This is why sellers are encouraged to clean up their properties beforehand and give the exteriors a bit of curb appeal.

How long does a home appraisal take?

The in-person home appraisal usually takes just a couple of hours to complete. But the whole appraisal process can take a few days to a week or longer, depending on the property and the appraiser’s schedule. In addition to a site visit, a licensed appraiser will research local market conditions, look at recent comparable sales, and evaluate property values in the area. They will also complete a written valuation report that is submitted to your mortgage lender.

What happens after a home appraisal?

After a home appraisal, an official appraised value is issued, and the home buying process continues. The lender will begin underwriting the mortgage loan, and, if approved, the buyer continues to the closing table where they present a cashier’s check or wire transfer for the down payment and other closing costs. If there is an issue with the appraisal, then the buyer and seller have an opportunity to renegotiate or terminate the purchase agreement.

What income is considered when applying for a mortgage?

Home buyers often have multiple income streams. Some have two part-time jobs, a full-time job, and a side hustle, contract work, gig work, or income from investment accounts. Others bring in cash from bonuses, commissions, or government-issued benefits.

Fortunately, mortgage lenders are happy to accept most income sources on your loan application, helping boost your qualifying income and your home-buying budget. But each income source will need to be verifiable and steady to qualify. Here’s what you should know before you apply.

Types of income that count towards a mortgage loan

There’s no definitive list of the income streams that qualify for a home loan. Each mortgage lender and loan program has its own requirements — including the types of income that qualify and the length of time you must have earned that income to be able to use it. Keep in mind that lenders are required by law to “make a reasonable, good faith determination of a consumer’s ability to repay” the mortgage loan.

To give you a good idea of the types of income that can commonly be used on a mortgage, we looked at Fannie Mae’s rulebook. Fannie Mae sets guidelines for conforming mortgages, which are the most popular type of home loan. So these requirements will apply to many home buyers.

Eligible income sources for a mortgage loan

Employee wages and salary income: Full-time employment is the most common type of income for home buyers. Expect to use documentation like recent pay stubs and one to two years of income tax returns to verify

Self-employed, freelance, and gig work income: Income in exchange for services that are outside of a traditional employment scenario. Anticipate needing at least two years of documentable history and tax returns

Part-time income: Similar to the requirements for full-time employment, but often two years of income history are needed

Tips: You’ll need to account for tip income with two years worth of documentation from either W2s or Form 4137

Bonuses and commissions: Your lender will likely use your average bonus or commission income over the last two years

Interest and dividend income: While generally eligible, there are some restrictions for investment income received for six months or less

Retirement, government, and pension income: Income from IRAs, 401K plans, pensions, and other retirement accounts are typically allowed

Social Security income: Lenders will often allow monthly payments to adults and children with low income or disabilities, as well as older adults age 65 and over

Disability payments: Unless benefits expire in the next three years, disability income is almost always eligible

Leave payments: Employer payments for paternity and maternity leave are usually permitted with a letter of explanation that details plan to return to work

Foster care payments: Usually allowed, but there are some documentation hurdles. Ask your lender about its requirements

Alimony and child support: These types of payments can often be included when they are regular and can be anticipated for three or more years to come

Trust income: Usually allowed when the applicant can show that payments will continue for several years after closing

Unemployment benefits: Although not typically eligible, seasonal workers who regularly claim benefits between seasons may be permitted

Rental or investment income: In some cases, proceeds from real estate investment property can be used with specialty lenders or some loan programs, like HomeReady

VA benefits: Similar to trust income, VA benefits are generally allowed provided that applicants can prove benefits will continue for the next several years

Military income: Allowances for housing and food, while either on base or deployed, can often be included as income

“In short, all income that is verifiable on your taxes”

Self-employment income

Self-employed mortgage borrowers typically need a two-year track record of successful earnings to apply for a mortgage. Lenders average the income if it’s going up, and take the lower figure (or worse) if it’s going down. You’ll also only be able to count your taxable income (after deductions), with a few exceptions for depreciation, depletion, and expenses that won’t recur.

Plan on providing your tax returns if you’re self-employed. And probably your latest financial statements and business license.

Bonuses and commissions

Generally, both bonuses and sales commissions can be taken into account by lenders. They typically consider bonus and commission income earned over the last two years. Lenders look at this income conservatively — if numbers are going up, they’ll average the income. If they are going down, however, the lender may use the lower figure. And if the industry you’re in is failing, lenders may discount income even more.

Part-time jobs

To count the income from an extra or part-time job, you’ll have to have been at it for at least one to two years. This also goes for seasonal work. For example, teaching skiing in the winter and golf in the summer would count if there’s a two-year history.

If you have a part-time job and a full-time job, you’re lender will likely want to see that you’ve worked both simultaneously for a year or two before applying. That’s because working two jobs can be strenuous, and lenders want to be certain you can manage the workload — and keep earning the extra income — consistently for years to come.

Tips

Your tips will be applicable to your lender’s income calculations as long as you’ve been getting them for two years. And you’ll have to back up your claims with documentation, including your last two IRS W-2 forms if your employer reports allocated tips, or Form 4137 if you report them yourself.

Investment Income

You should be able to count investment income — including interest and dividends — in full on your mortgage application However, the amount you can use as income for mortgage purposes will be an average of your last two years’ receipts. If you plan to liquidate any of those assets for your down payment or closing costs, you can expect your lender to deduct their income.

Retirement, government, annuity, and pension income

If your retirement includes savings in an IRA, 401(k), or other retirement accounts, you can use it as income to qualify for a mortgage.

Underwriters start with 70% of your retirement balances to account for fluctuations in the values of stocks and bonds (cash deposits are not subject to this). They then divide your total by the number of months in your mortgage. So if you take a 30-year loan, they divide by 360. If you want a 15-year loan, they divide by 180. That number is your income for the month from what lenders call “asset depletion.”

Social Security income

If you’re getting Social Security income from the government, including retirement or long-term disability benefits, it should normally be accepted as income for mortgage purposes. It’s a bit more complicated when you’re receiving benefits on behalf of a family member. Then, you’ll have to show the income will continue for at least the next three years.

Maternity and paternity leave

Provided you write to your lender, confirming that you will return to work on a particular date, you’ll typically be fine. Your normal employment income will usually continue to apply, even if you’re on a reduced salary or will be unpaid at closing. However, you’ll need a pile of paperwork, including correspondence from your employer confirming your return-to-work date.

Disability benefits

If you receive disability income, it can typically be used on your mortgage application. Long-term disability benefits from sources other than the Social Security Administration almost always count. Short-term disability benefits may also count, depending on how close their expiration date is. If you’re going to transition from short-term to long-term within the next three years, expect only the long-term benefits to be included in your lender’s calculations.

Foster care

Fannie Mae likes you to have been receiving income from fostering for two years. However, it may accept one year, providing the relevant income is 30% or less of your total gross income.

Alimony and child support

Alimony and child support payments can count as income for a mortgage, but only if the payments are consistent. If your ex-spouse doesn’t make regular alimony or child support payments, you may not be able to count that income. Not even if you have a watertight court order or separation agreement. Because you’ll have to show you’ve received “full, regular and timely” payments going back at least six months.

Also, lenders will look at how long you can expect to receive child support. Suppose your child is 16 years old. And that your child support’s going to end when they’re 18. You can’t count that support toward your income for mortgage purposes, because qualifying income must continue for at least three years. Of course, if you have younger kids who will be supported for three or more years, their child support will still count.

Trust income

If you’re the beneficiary of a trust, that money should be applicable income for mortgage purposes. You’ll have to show that you’ll receive it for at least three years. And the lender will need a copy of the trust documents confirming the frequency, amount, and duration of the payments.

Unemployment benefits

You’re unlikely to get a mortgage on unemployment income because unemployment benefits are intended to be temporary by nature. But unemployment income may count if you’re a seasonal worker who regularly claims those benefits between jobs. Your lender will want to see that you’ve been getting benefits and working in this way for a couple of years. And it will verify that you can reasonably expect the pattern to continue.

VA benefits

VA benefits should normally count for a mortgage. All you have to do is prove you’re getting them and show they’ll last for at least the next three years. You won’t have to provide that verification if you’re receiving your benefits owing to retirement or long-term disabilities.

Rental income

Rent from boarders generally counts as income for mortgage purposes only with some specialty programs, such as Fannie’s HomeReady loan. However, there is an exception. That’s when you have disabilities and your personal assistant lives in and pays you (or maybe Medicare Waiver funds pay you) for their accommodation. Still, you can only count 30% of that rent as income.

“Grossing up” income

Some kinds of income are not subject to taxes. For example, child support and disability. In that case, lenders are allowed to count that income as worth more. Usually, non-taxable income is worth 25% more for mortgage qualifying. So, $1,000 a month in child support counts as $1,250 a month. They call this practice “grossing up” income because you’ll actually have more after-tax income. “This is most often done with retirement income, such as Social Security,” adds Meyer.

Why mortgage companies care about income sources

Many first-time home buyers won’t have to worry much about multiple income sources. Chances are, you have pretty straightforward finances. Indeed, for many, a single income stream from one employer is all they have — and all they need.

But others have multiple streams from different sources. Or one stream made up of different elements. In this case, approval can be a little more complicated. That’s because the lender has to verify each income stream individually to ensure you’ll continue at the same total income level for years to come. Remember that a mortgage lender’s ultimate goal is to make sure you can afford your home loan payments for many years into the future.

Ability to repay

All lenders have a legal obligation to “make a reasonable, good faith determination of a consumer’s ability to repay any consumer credit transaction secured by a dwelling.” In other words, they must examine your finances in detail. Because they must make sure you can comfortably afford your monthly mortgage payments, home equity loan, or home equity line of credit (HELOC).

This is called the “ability to repay” provision. It protects against predatory lending to people who have little chance of repaying their mortgages.

Income rules and rule makers

Mortgage lenders all have the same legal obligation to ensure your ability to repay. But some interpret that duty differently. So if you’re turned down by one lender, it may be worth trying others.

If you want a government-backed home loan, the rules on income for mortgage qualification are written pretty tightly. Those government-backed mortgages include Federal Housing Administration (FHA) loans, Department of Veterans Affairs (VA) loans, and U.S. Department of Agriculture (USDA) loans.

Fannie Mae and Freddie Mac also closely specify the income streams they’re prepared to accept for conventional loans. However, those aren’t chiseled in stone. Conventional mortgages may be more flexible when it comes to income qualifying than government-backed mortgages.

Rules may vary by lender and loan program

In very exceptional circumstances, lenders may bend some income rules for favored borrowers. For example, suppose you’ve been with a local institution for decades. If it knows you have an unblemished payment record and a stellar credit score, it may be willing to bend policy a little.

Equally, Fannie and Freddie write their rules for particular mortgage products. For example, Fannie usually excludes rental income from a mortgage application. But it makes an exception for its HomeReady mortgage. If you apply for one of those, Fannie can count all the income you receive from boarders and renters, provided they’ve lived with you for at least a year prior to buying the home.

What counts as income for a mortgage refinance loan?

If you’re a homeowner looking to refinance your current mortgage, you face the same income requirements as home buyers. You can use a wide variety of income sources to qualify but you must show a steady history of receiving that income. And lenders must be able to ensure it will continue in the future. You will have to prove any income sources using tax forms, bank and investment account statements, pay stubs, and other standard documentation.

Other factors that matter when qualifying for a mortgage

You’ll need more than qualifying income to get approved for a mortgage application. Lenders look at a variety of factors. These include:

Debt-to-income ratio (DTI): Lenders use your DTI ratio to compare your total monthly debt to your gross monthly income. This shows the economic burden on your household finances. Debt can include payments on car loans, student loans, and credit card payments, to name a few. The lower your DTI ratio, the better your chances of mortgage approval

Credit score: You’ll generally need a credit score of 620 or higher to qualify for a conventional loan, but some first-time home buyers can qualify for an FHA loan with scores as low as 580

Down payment: Most borrowers will need at least 3% down for conventional mortgages and 3.5% down for FHA loans. Keep in mind that you’ll pay private mortgage insurance (PMI) without 20% down on a conventional loan. And mortgage insurance premiums (MIP) is required on an FHA loan, regardless of the down payment amount. Both USDA and VA loans require no down payment whatsoever

Asset and cash reserves: Many lenders and loan programs want buyers to have adequate cash reserves or emergency funds after closing on a new home. This shows that you’ll be able to make your monthly mortgage payments in the event that your income ceases

Today’s mortgage rates

The above examples are a broad overview of what can count as income for mortgage purposes. There’s a whole lot more detail, so talk to your lender about what rules apply.

Remember that there is a legal obligation on lenders to ensure your home loan will be affordable. They’re going to vet every income source thoroughly. So begin getting together your paperwork early.

In the meantime, you can review your current home-buying options using the link below. It’s free to compare interest rates from multiple lenders, and you are under no obligation to act.

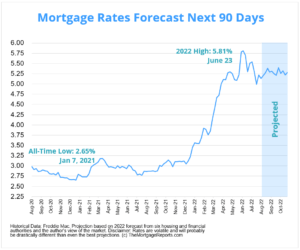

Mortgage rate forecast for next week (Sept. 26-30)

Mortgage rates grew for the fourth week in a row and broke 6% for the first time since 2008.

The average 30-year fixed interest rate rose from 5.89% on Sept. 8 to 6.02% on Sept. 15, according to Freddie Mac.

With another week of growth, the lending market continues to make adjustments for the large Federal Reserve hike likely coming at the end of the month. The Fed keeps signaling aggressive policy actions in order to bring inflation down to normal levels.

Will mortgage rates go down in September?

Mortgage rates fluctuated greatly so far in the third quarter of 2022, with the average 30-year fixed rate dipping as low as 4.99% on Aug. 4 to a high-water mark of 6.02% on Sept. 15, according to Freddie Mac.

This followed 248 basis points (2.48%) of growth in the year’s first half. Rates varied from one week to the next as the Fed wrestled with inflation. Mortgage rates experienced the largest weekly jump since 1987, surging 55 basis points (0.55%) the day after the Federal Reserve’s June hike.

With the pandemic’s declining economic impact, decades-high inflation, and the Fed planning three more aggressive hikes, interest rates could continue trending upward this year.

However, concerns over an impending recession have caused rate drops and could cause more on any given week.

Experts from Attom Data Solutions, CoreLogic, Realtor.com and other industry leaders are split on whether 30-year mortgage rates will keep climbing in September or level off.

“If fears of recession outweigh fears of inflation, mortgage rates may come down.”

–Odeta Kushi, deputy chief economist at First American

Expert mortgage rate predictions for September

Paul Buege, chief executive officer and president at Inlanta Mortgage

Prediction: Rates will rise

“I think we’re going to be range-bound and we’ll see rates stay at this level, maybe a little bit higher. The market is responding to the Fed’s two significant rate increases and the economy is cooling. What you’re seeing right now is the initial response: a recession and people aren’t buying as much.

But always lurking in the background is going to be some economic news showing that things haven’t cooled to the level that you might think. That’s why I think you’re gonna have these little rate bumps up and down. If you wanted to work with a really broad range, probably 6% would be the high and 5% might be the low. That’s what we’re using as we manage our book of business as a company.”

“There isn’t a Fed meeting [in August] but there is the annual economic policy symposium in Jackson Hole that a lot of the Fed decision makers participate in. Investors will look to that symposium to get an updated sense of how the Fed is thinking about monetary policy and we may see mortgage rates react to whatever is discussed.

Even though the Fed is still tightening policy, inflation is moving back in the direction that we want to see. I think that means we’re going to see a bit more volatility in mortgage rates in the next year. The fact they’ve come down from 5.8% suggests that investors believe the Fed may not have to increase short-term rates as high as they thought two months ago. Watching those inflation numbers is key to getting an idea of where mortgage rates might go moving forward.”

“Mortgage rates will likely remain around 5.5% in September. While the highly-anticipated Fed meeting will take place in September, the mortgage market has likely already accounted for all of the expected increase in the funds rate in 2022 prior to the June meeting, when mortgage rates jumped to 6%. The decrease in rates since then reflects the adjustment to slowing home buying demand and widening economic uncertainty.

Borrowers should be in a better position to get a more favorable rate than in June. Also, borrowers have increasingly turned to adjustable-rate mortgages which provide some relief with monthly mortgage expenditures. Borrowers in a position to do so could help lower their rates by coming up with larger down payments.”

Odeta Kushi, deputy chief economist at First American

Prediction: Rates will moderate

“Ongoing concerns about the economy and the Federal Reserve’s fight against inflation may prompt mortgage rates to follow a seesaw trend in September. While some agree that inflation may have peaked, it remains uncomfortably high, which puts the Fed in a position to continue interest rate hikes.

Going forward, if fears of recession outweigh fears of inflation, mortgage rates may come down. However, if inflation surprises to the upside, the Fed will likely take more aggressive action and mortgage rates will climb faster as a result. Ultimately, how the market interprets incoming data leading up to the September Federal Open Market Committee (FOMC) meeting will have a strong impact on how mortgage rates respond in September.”

Jessica Lautz, VP of demographics and behavioral insights at National Association of Realtors

Prediction: Rates will moderate

“There seems to currently be some leveling off of the recent rise in mortgage interest rates. Inflation plays the key role in what happens next, but it’s possible we are at a plateau for mortgage interest rates.

Consumers should talk to a few mortgage brokers. Different brokers may be familiar with home loan products that help buyers with their first home loan.”

Rick Sharga, EVP of market intelligence at Attom Data Solutions

Prediction: Rates will moderate

“It appears that the market has already “baked in” rate hikes from the Federal Reserve — that may have something to do with the sudden jump in rates even before we saw the Fed dramatically raise Fed Funds rates.

I don’t expect September mortgage rates to behave much differently than what we’re seeing right now — we’ll probably continue to see rates on 30-year fixed-rate loans ranging between 5% and 5.50% over the course of the month, unless we get any unexpectedly negative economic news.

Another thing to consider is home sales have dropped significantly as mortgage rates have risen — 15% in June, which marked the sixth consecutive month of decreasing sales. We may be seeing some rate competition among lenders in an attempt to make home purchases slightly more affordable for buyers and to generate more purchase loan activity. While lenders certainly can’t control interest rates, they can nibble at the margins, perhaps sacrificing some profit in order to secure more volume.”

Mortgage interest rates forecast next 90 days

The Federal Reserve made an aggressive policy plan to bring inflation down. While that would normally lead to mortgage rate growth, the lending market may have already accounted for the Fed’s rate hikes.

Because of this, many experts currently believe mortgage interest rates will move within a tighter range in the fall compared to the big weekly swings we saw throughout the year.

Of course, the Russian-Ukrainian war or a new wave of Covid-19 could create economic uncertainty and cause more rate volatility in the coming months.

Mortgage rate predictions for 2022

The average 30-year fixed-rate mortgage ended the second quarter of 2022 at 5.7%, according to Freddie Mac.

Five of the six major housing authorities we gathered project the average for the third quarter to drop below that.

Fannie Mae and the National Association of Home Builders sit at the low end of the group, estimating the average 30-year fixed interest rate will settle below 5.2% by the end of Q3. Meanwhile, Freddie Mac and the National Association of Realtors had the highest predictions, with forecasts of 5.5% and 5.8%, respectively, by the end of September.

Housing Authority

30-Year Mortgage Rate Forecast (Q3 2022)

Fannie Mae

5.10%

National Association of Home Builders

5.19%

Mortgage Bankers Association

5.20%

Wells Fargo

5.20%

Freddie Mac

5.50%

National Association of Realtors

5.80%

Average Prediction

5.33%

Current mortgage interest rate trends

With the September Fed meeting approaching and another big hike expected, average mortgage rates climbed for the fourth week in a row.

The average 30-year fixed rate shot up from 5.89% to 6.02% for the seven days ending Sept. 15, according to Freddie Mac’s weekly rate survey.

Similarly, the 15-year fixed rate rose from 5.16% to 5.21%, and the average rate for a 5/1 ARM jumped from 4.64% to 4.93%.

Month

Average 30-Year Fixed Rate

August 2021

2.84%

September 2021

2.90%

October 2021

3.07%

November 2021

3.07%

December 2021

3.10%

January 2022

3.45%

February 2022

3.76%

March 2022

4.17%

April 2022

4.98%

May 2022

5.23%

June 2022

5.52%

July 2022

5.41%

Source: Freddie Mac

Mortgage rates moved on from the record–low territory seen in 2020 and 2021 but are still below average from a historical perspective.

Dating back to April 1971, the fixed 30–year interest rate averaged around 7.8%, according to Freddie Mac. So if you haven’t locked a rate yet, don’t lose too much sleep over it. You can still get a great deal, historically speaking — especially if you’re a borrower with strong credit.

Just make sure you shop around to find the best lender and lowest rate for your unique situation.

Mortgage rate trends by loan type

Many mortgage shoppers don’t realize there are different types of rates in today’s mortgage market. But this knowledge can help home buyers and refinancing households find the best value for their situation.

Following are 3-month mortgage rate trends for the most popular types of home loans: conventional, FHA, VA, and jumbo.

July 2022

June 2022

May 2022

Conforming Loan Rates

5.30%

5.79%

5.34%

FHA Loan Rates

5.27%

5.59%

5.25%

VA Loan Rates

5.00%

5.34%

4.95%

Jumbo Loan Rates

5.02%

5.34%

4.92%

Source: Black Knight Originations Market Monitor Report

Which mortgage loan is best?

The best mortgage for you depends on your financial situation and your goals.

For instance, if you want to buy a high–priced home and you have great credit, a jumbo loan is your best bet. Jumbo mortgages allow loan amounts above conforming loan limits, which max out at $647,200 in most parts of the U.S.

On the other hand, if you’re a veteran or service member, a VA loan is almost always the right choice. VA loans are backed by the U.S. Department of Veterans Affairs. They provide ultra-low rates and never charge private mortgage insurance (PMI). But you need an eligible service history to qualify.

Conforming loans and FHA loans (those backed by the Federal Housing Administration) are great low–down–payment options.

Conforming loans allow as little as 3% down with FICO scores starting at 620. FHA loans are even more lenient about credit; home buyers can often qualify with a score of 580 or higher, and a less–than–perfect credit history might not disqualify you.

Finally, consider a USDA loan if you want to buy or refinance real estate in a rural area. USDA loans have below-market rates — similar to VA — and reduced mortgage insurance costs. The catch? You need to live in a ‘rural’ area and have moderate or low income to be USDA–eligible.

Mortgage rate strategies for September 2022

Mortgage rates grew fast and furiously to open in 2022. The pace slowed in the second quarter, then interest rates shot up after the Fed’s 0.75% federal funds rate hike in mid-June. The central bank said it anticipates multiple similar hikes in 2022. Mortgage rates could climb throughout the rest of the year as a means to offset inflation. However, opportunities to lock in a low-interest rate do still exist for home buyers and refinancing homeowners.

Here are just a few strategies to keep in mind if you’re mortgage shopping in the coming months.

Have a plan — and stick to it

“Don’t doom scroll, don’t get too seduced by the headlines. It can be tough for the first-time home buyer, but it also doesn’t have to be if you have a plan.”

-Paul Buege, chief executive officer and president at Inlanta Mortgage

Between ballooning prices and a lack of listings, home buying in 2022 has been tough and likely even frustrating for many borrowers. However, conditions are beginning to ease.

With listings sitting on the market longer and interest rates possibly peaked, now’s not the time to give up or be erratic with your money. Much like playing at a blackjack table, your best bet at winning — or in this case, buying a home — comes with sticking to a consistent strategy and patience.

“Don’t doom scroll, don’t get too seduced by the headlines. It can be tough for the first-time home buyer, but it also doesn’t have to be if you have a plan,” Buege said. “If someone wants to buy a home, you can, it just might be at a different time than what you’re hoping. But I think things are cooling down. We really try to advise everyone to respect the market. Virtually everything that’s going on out there is outside all of our control.”

So figure out when you want to buy a home, prepare yourself, and know all the borrower requirements. While affordability took a hit over the last few years, you can still get creative and find ways to save money.

Work for a lower interest rate

One of the biggest parts of home buying is the mortgage rate you’re able to lock into. Everyone wants the lowest possible interest rate they can get but that’s mostly determined by what the lending market offers on a given day. Unfortunately, timing isn’t always in every borrower’s favor.

That’s where mortgage discount points come in. It’s a lever borrowers can pull to decrease their monthly mortgage costs and paying down your rate could save thousands of dollars over the life of your home loan.

“Rather than asking the seller to drop their price, a buyer can leverage a seller concession to buy down their mortgage rate via points,” said Taylor Marr, deputy chief economist at Redfin. “This will have a much greater impact on lowering their monthly mortgage payment than a lower [home purchase] price would.”

Although, paying for mortgage points adds more upfront costs at closing, which could be a barrier to entry for some borrowers. Shopping your rate around by contacting multiple lenders to see if they can offer a lower one only requires time and effort. Given how lenders differ and how volatile interest rates tend to be, taking your first offer could be a mistake.

How to shop for interest rates

Rate shopping doesn’t just mean looking at the lowest rates advertised online because those aren’t available to everyone. Typically, those are offered to borrowers with perfect credit and who can put a down payment of 20% or more.

The rate lenders actually offer depends on:

Your credit score and credit history

Your personal finances

Your down payment (if buying a home)

Your home equity (if refinancing)

Your loan-to-value ratio (LTV)

Your debt-to-income ratio (DTI)

To figure out what rate a lender can offer you based on those factors, you have to fill out a loan application. Lenders will check your credit and verify your income and debts, then give you a ‘real’ rate quote based on your financial situation.

You should get three to five of these quotes at a minimum, then compare them to find the best offer. Look for the lowest rate, but also pay attention to your annual percentage rate (APR), estimated closing costs, and ‘discount points’ — extra fees charged upfront to lower your rate.

This might sound like a lot of work. But you can shop for mortgage rates in under a day if you put your mind to it. And shaving just a few basis points off your rate can save you thousands.

Mortgage interest rate FAQ

What are current mortgage rates?

Current mortgage rates are averaging 6.02% for a 30–year fixed–rate loan, 5.21% for a 15–year fixed–rate loan, and 4.93% for a 5/1 adjustable–rate mortgage, according to Freddie Mac’s latest weekly rate survey. Your individual rate could be higher or lower than the average depending on your credit score, down payment, and the lender you choose to work with, among other factors.

Will mortgage rates go down next week?

Mortgage rates could decrease next week (Sept. 26-30, 2022) if the mortgage market takes a cautious approach to a possible recession. However, rates could rise if lenders continue to account for the Federal Reserve taking more aggressive measures to counteract the high inflation of 2022.

Will mortgage interest rates go down in 2022?

It’s unlikely mortgage rates will go down in 2022. Inflation has been climbing at a record rate over the last few months. And the Fed is planning to raise interest rates after each of its scheduled FOMC meetings. Both these factors should lead to significantly higher mortgage rates in 2022.

Will mortgage interest rates go up in 2022?

Yes, it’s very likely mortgage rates will increase in 2022. High inflation, a strong housing market, and policy changes by the Federal Reserve should all push rates higher in 2022. The only thing likely to push rates down would be a major resurgence in serious Covid cases and further economic shutdowns. But, while it could help mortgage rates, no one is hoping for that outcome.

What is the lowest mortgage rate right now?

Freddie Mac is now citing average 30-year rates in the 5 percent range. If you can find a rate in the 4s, you’re in a very good position. Remember that rates vary a lot by borrower. Those with perfect credit and large down payments may get below-average interest rates, while poor-credit borrowers and those with non-QM loans could see much higher rates. You’ll need to get pre-approved for a mortgage to know your exact rate.

Will there be a housing crash in 2022?

For the most part, industry experts do not expect the housing market to crash in 2022. Yes, home prices are over-inflated. But many of the risk factors that led to the 2008 crash are not present in today’s market. Low inventory and massive buyer demand should keep the market propped up next year. Plus, mortgage lending practices are much safer than they used to be. That means there’s not a subprime mortgage crisis waiting in the wings.

What is the lowest mortgage rate ever?

At the time of this writing, the lowest 30-year mortgage rate ever was 2.65 percent. That’s according to Freddie Mac’s Primary Mortgage Market Survey, the most widely used benchmark for current mortgage interest rates.

Should I lock my rate now or wait?

Locking your rate is a personal decision. You should do what’s right for your situation rather than trying to time the market. If you’re buying a home, the right time to lock a rate is after you’ve secured a purchase agreement and shopped for your best mortgage deal. If you’re refinancing, you should make sure you compare offers from at least three to five lenders before locking a rate. That said, rates are rising. So the sooner you can lock in today’s market, the better.

Is now a good time to refinance?

That depends on your situation. It’s a good time to refinance if your current mortgage rate is above market rates and you could lower your monthly mortgage payment. It might also be good to refinance if you can switch from an adjustable-rate mortgage to a low fixed-rate mortgage; refinance to get rid of FHA mortgage insurance; or switch to a short-term 10- or 15-year mortgage to pay off your loan early.

Is it worth refinancing for 1 percent?

It’s often worth refinancing for 1 percentage point, as this can yield significant savings on your mortgage payments and total interest payments. Just make sure your refinance savings justify your closing costs. You can use a mortgage calculator or speak with a loan officer to crunch the numbers.

How do I shop for mortgage rates?

Start by choosing a list of three to five mortgage lenders that you’re interested in. Look for lenders with low advertised rates, great customer service scores, and recommendations from friends, family, or a real estate agent. Then get pre-approved by those lenders to see what rates and fees they can offer you. Compare your offers (Loan Estimates) to find the best overall deal for the loan type you want.

What are today’s mortgage rates?

Mortgage rates are rising, but borrowers can usually find a better deal by shopping around. Connect with a mortgage lender to find out exactly what rate you qualify for.

Average mortgage rates edged modestly higher yesterday, setting another 14-year high. So far this week, we’ve seen three modest rises, one big one and no falls.

By approaching 10 a.m. (ET), markets were signaling that mortgage rates today could fall. That would make a welcome change. But, as always, things might change as the hours pass.

Find your lowest rate. Start here (Sep 16th, 2022)

Current mortgage and refinance rates

Program

Mortgage Rate

APR*

Change

Conventional 30 year fixed

6.311%

6.34%

+0.05%

Conventional 15 year fixed

5.612%

5.651%

+0.1%

Conventional 20 year fixed

6.445%

6.503%

+0.03%

Conventional 10 year fixed

5.552%

5.669%

+0.02%

30 year fixed FHA

6.392%

7.264%

+0.09%

15 year fixed FHA

6.053%

6.616%

+0.08%

30 year fixed VA

6.013%

6.24%

+0.3%

15 year fixed VA

6.125%

6.483%

Unchanged

Should you lock a mortgage rate today?

Don’t lock on a day when mortgage rates look set to fall. My recommendations (below) are intended to give longer-term suggestions about the overall direction of those rates. So, they don’t change daily to reflect fleeting sentiments in volatile markets.

Although there are bound to be plenty of rises and falls over the next three months, I suspect the overall direction of travel will be gently upward.

So, my personal rate lock recommendations remain:

LOCK if closing in 7 days

LOCK if closing in 15 days

LOCK if closing in 30 days

LOCK if closing in 45 days

LOCK if closing in 60 days

Market data affecting today’s mortgage rates

Here’s a snapshot of the state of play this morning at about 9:50 a.m. (ET). The data, compared with roughly the same time yesterday, were:

The yield on 10-year Treasury notes nudged up to 3.48% from 3.45%. (Bad for mortgage rates.) More than any other market, mortgage rates normally tend to follow these particular Treasury bond yields

Major stock indexes were falling soon after opening. (Sometimes good for mortgage rates.) When investors are buying shares, they’re often selling bonds, which pushes prices of those down and increases yields and mortgage rates. The opposite may happen when indexes are lower. But this is an imperfect relationship

Oil prices decreased to $85.30 from $85.77 a barrel. (Good for mortgage rates*.) Energy prices play a prominent role in creating inflation and also point to future economic activity

Goldprices dropped to $1,666 from $1,691 an ounce. (Bad for mortgage rates*.) It is generally better for rates when gold rises and worse when gold falls. Gold tends to rise when investors worry about the economy. And worried investors tend to push rates lower

CNN Business Fear & Greed index — tumbled to 34 from 41 out of 100. (Good for mortgage rates.) “Greedy” investors push bond prices down (and interest rates up) as they leave the bond market and move into stocks, while “fearful” investors do the opposite. So lower readings are better than higher ones

*A movement of less than $20 on gold prices or 40 cents on oil ones is a change of 1% or less. So we only count meaningful differences as good or bad for mortgage rates.

Caveats about markets and rates

Before the pandemic and the Federal Reserve’s interventions in the mortgage market, you could look at the above figures and make a pretty good guess about what would happen to mortgage rates that day. But that’s no longer the case. We still make daily calls. And are usually right. But our record for accuracy won’t achieve its former high levels until things settle down.

So use markets only as a rough guide. Because they have to be exceptionally strong or weak to rely on them. But, with that caveat, mortgage rates today look likely to fall. However, be aware that “intraday swings” (when rates change direction during the day) are a common feature right now.

Find your lowest rate. Start here (Sep 16th, 2022)

Important notes on today’s mortgage rates

Here are some things you need to know:

Typically, mortgage rates go up when the economy’s doing well and down when it’s in trouble. But there are exceptions. Read ‘How mortgage rates are determined and why you should care

Only “top-tier” borrowers (with stellar credit scores, big down payments, and very healthy finances) get the ultralow mortgage rates you’ll see advertised

Lenders vary. Yours may or may not follow the crowd when it comes to daily rate movements — though they all usually follow the broader trend over time

When daily rate changes are small, some lenders will adjust closing costs and leave their rate cards the same

Refinance rates are typically close to those for purchases.

A lot is going on at the moment. And nobody can claim to know with certainty what will happen to mortgage rates in the coming hours, days, weeks or months.

Are mortgage and refinance rates rising or falling?

Regular readers will have been surprised by countless headlines yesterday. Take one in The Wall Street Journal (paywall) as an example: “Mortgage Rates Top 6% for the First Time Since the 2008 Financial Crisis.” That message was repeated in similar forms by endless news outlets.

But hang on! Haven’t average mortgage rates (meaning those for conventional, 30-year, fixed-rate mortgages) been above 6% for all but two days this month? And weren’t they over 6% for a while in June?

Well, yes. But all those headlines were generated by Freddie Mac’s latest weekly rates report. And that’s flawed in a couple of ways.

Most relevantly, it assumes that you’re going to buy discount points on closing that earn you a lower rate. Right now, that’s often a very smart move because there are real bargains out there.

But not everyone can afford them. And assuming that everyone purchases points skew the rates Freddie publishes, making them lower.

We think you deserve a clearer picture. So, we publish raw average rates that don’t make assumptions about whether you’re able and willing to buy discount points.

If you’re one of the lucky ones who can and do purchase points, you’ll get a nice surprise when you receive your quotes. If you’re not, you won’t get a nasty shock.

Today

After an exhausting week for economic reports, today’s relatively quiet. It brings two reports from the University of Michigan: the consumer sentiment index and the 5-year consumer inflation expectations report.

Normally, those rarely move mortgage rates. But, in today’s febrile markets, they just might — though probably only modestly unless they’re truly shocking. Higher-than-expected figures for either might push up those rates while lower ones might drag them down.

Further ahead

Next week’s economic reports are mostly about real estate. But next Wednesday will almost inevitably see Federal Reserve Chair Jerome Powell unveil another rate hike.

CME FedWatch puts the chances of a third consecutive 75-basis-point (0.75%) rise at 74%. But it reckons there’s a 26% chance of a huge 100-basis-point (1%) hike. In the event of the latter being announced, expect sharply higher mortgage rates.

Why do I keep mentioning basis points? Because it clears up possible confusion. A 1% rise might mean an increase of y x 1%, or it might mean y + 1%. Suppose you’re looking at a 3% rate. That 3% x 1% is a 0.03% hike to 3.03%. But 3% + 1% = 4%, a much bigger jump. By mentioning basis points I’m clarifying that I’m talking about the latter.

Recent trends

Over much of 2020, the overall trend for mortgage rates was clearly downward. And a new, weekly all-time low was set on 16 occasions that year, according to Freddie Mac.

The most recent weekly record low occurred on Jan. 7, 2021, when it stood at 2.65% for 30-year fixed-rate mortgages.

Freddie’s Sep. 15 report put that same weekly average for conventional, 30-year, fixed-rate mortgages at 6.02% (with 0.8 fees and points), up from the previous week’s 5.89%. Little of that Tuesday’s big rise is likely to be reflected in Freddie’s latest report.

Note that Freddie expects you to buy discount points (“with 0.8 fees and points”) on closing which earns you a lower rate. If you don’t do that, your rate would be closer to the ones we and others quote.

Expert mortgage rate forecasts

Looking further ahead, Fannie Mae, Freddie Mac, and the Mortgage Bankers Association (MBA) each have a team of economists dedicated to monitoring and forecasting what will happen to the economy, the housing sector and mortgage rates.

And here are their current rate forecasts for the remaining two quarters of 2022 (Q3/22, Q4/22) and the first two quarters of next year (Q1/23, Q2/23).

The numbers in the table below are for 30-year, fixed-rate mortgages. Fannie’s forecast appeared on Aug. 22 and the MBA’s on Aug. 23. Freddie’s came out around Jul. 21. But it now releases forecasts only quarterly. So, expect its figures to look stale soon.

Forecaster

Q3/22

Q4/22

Q1/23

Q2/23

Fannie Mae

5.1%

4.8%

4.7%

4.5%

Freddie Mac

5.5%

5.4%

5.2%

5.2%

MBA

5.3%

5.2%

5.1%

5.0%

Of course, given so many unknowables, the whole current crop of forecasts might be even more speculative than usual. And their past record for accuracy hasn’t been wildly impressive. Personally, I think they’re too optimistic.

Find your lowest rate today

You should comparison shop widely, no matter what sort of mortgage you want. As a federal regulator the Consumer Financial Protection Bureau says:

“Shopping around for your mortgage has the potential to lead to real savings. It may not sound like much, but saving even a quarter of a point in interest on your mortgage saves you thousands of dollars over the life of your loan.”

Mortgage rate methodology

We arrive at an average rate and APR for each loan type to display in our chart. Because we average an array of rates, it gives you a better idea of what you might find in the marketplace. Furthermore, we average rates for the same loan types. For example, FHA fixed with FHA fixed. The end result is a good snapshot of daily rates and how they change over time.